Calculating the Return on Investment of the CFPB

The CFPB - the Consumer Financial Protection Bureau - was established in 2010, by Act of Congress, under and with the strong support of the Obama Administration. To remind you: this was in the dark shadow of the 2007 - 2009 financial collapse. One of the particular horrors was that many ordinary home owners got into deep financial trouble with mortgages for homes they could not afford and would not have bought but for the presence of mortgages at low teaser rates. When these rates ratcheted up to market rates and home prices collapsed, about six million households lost their homes to foreclosure with foreclosures running at about ten times normal rates.

So, the CFPB was built as a focal point, bringing together functions that had existed throughout the Federal Government, adding some new ones, and giving it a combined mission - informing and defending individual or small business consumers. This from its mission statement - protecting “consumers from unfair, deceptive, or abusive practices and (taking) action against companies that break the law. (arming) people with the information, steps, and tools that they need to make smart financial decisions." (Oxford commas in the original.)

The CFPB's unique and powerful structure has long made it a controversial agency, including the breadth of its remit and that the Bureau’s funding comes from the Federal Reserve bank, not from Congressional allocation. To critics, the breadth and growth of the Bureau’s mandate and the constraints on its oversight make a powerful and perhaps dangerous combination. (Cato podcast discussion here.) Nonetheless, the Supreme Court accepted the Bureau’s funding and oversight structure in 2024.

On February 9th, 2025, incoming CFPB chief operating officer Adam Martinez “instructed staff to suspend nearly all activities of the regulator, including supervising financial firms." The following day, this message was reiterated in a memo from Project 2025 lead and incoming CFPB director Russell Vought, saying that “employees needed clearance from chief legal officer Mark Paolette to do anything related to CFPB business.” (Quoted text from CNBC here)

Our simple questions here are:

- How much does CFPB cost?

- What benefits are returned to consumers, the citizens, business, allies, and others in the USA?

- What downstream harms has it caused. (We note that there can be external harms from the operation of the CFPB, although writings to date see these mostly as theoretical rather than demonstrated.)

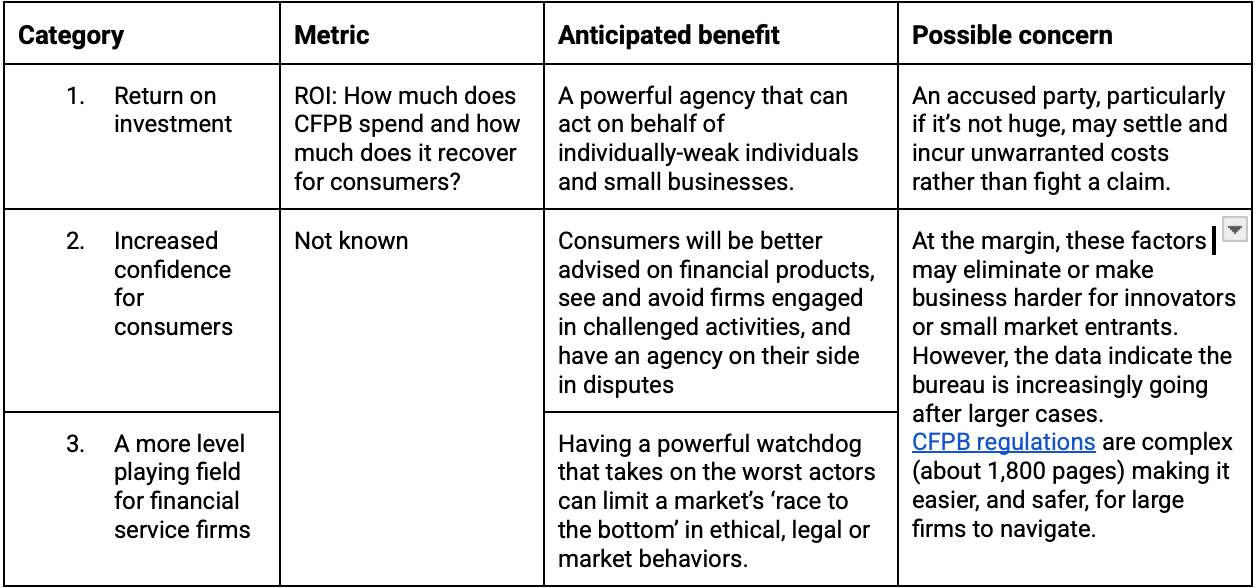

One can imagine the benefits falling into three categories, and possible problems caused by the agency along the way. Here’s a simple summary of these categories. One thing is easy to see: intangible downstream harms are hard to quantify.

CFPB Benefits and Possible Concerns

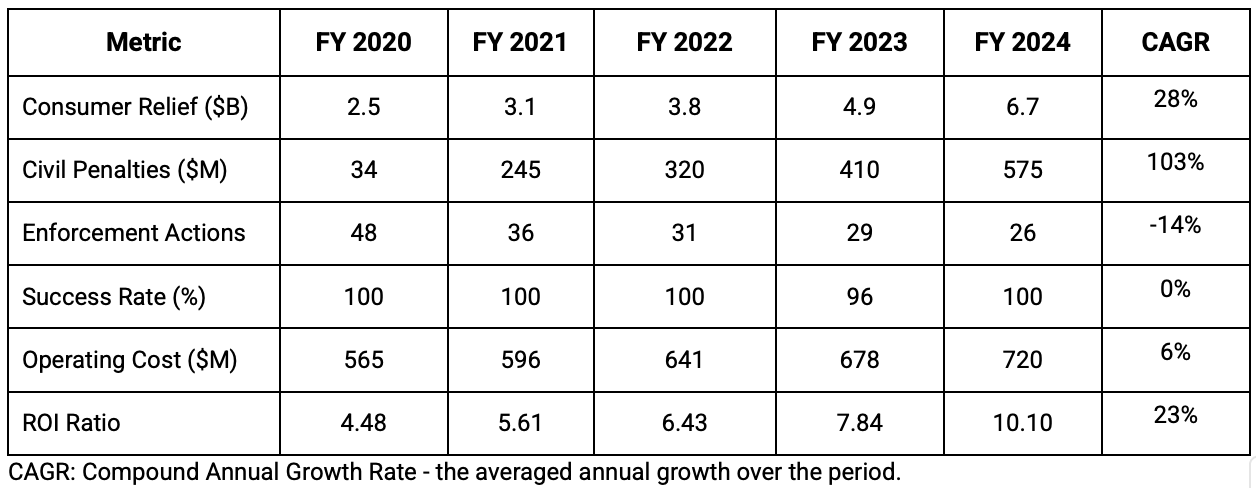

Only one of these benefits can be readily calculated from publicly-available materials: the ROI. From this, it seems that CFPB is returning to consumers significantly more than it costs taxpayers to maintain the bureau - and the ratio is increasing.

CFPB ROI (FY 2020-2024)

About this table:

- Consumer Relief: This represents the amount of monetary compensation, principal reductions, canceled debts, and other consumer relief resulting from CFPB enforcement and supervisory work.

- Civil Penalties: These are fines imposed on companies and individuals that violate consumer financial protection laws.

- Enforcement Actions: The number of public enforcement actions concluded by the CFPB each year. The decreasing trend (number down by 14% per year) against a 23% annual increase in recovery indicates the bureau moving toward larger, more focused, high-impact actions.

- Success Rate: The percentage of enforcement actions successfully resolved through litigation, settlement, or default judgment.

- Operating Cost: An estimate of the CFPB's annual budget, which has grown modestly over the years.

- ROI Ratio: Calculated as (Consumer Relief + Civil Penalties) / Operating Cost. This shows how much value the CFPB generates for consumers relative to its operational expenses. A challenge here is that both costs and recoveries are recorded in each year, whereas in reality the timing of recoveries typically lag incurral of costs by a significant period, depending on case complexity. This would imply that actual return rates could be even higher than implied by the table.

Bottom lines

If the ratio of funds returned to consumers over the cost to taxpayers - here, the ROI - is the bottom line, then it seems highly beneficial. $1 in CFPB spending in 2000 yielded nearly $4.5 for consumers; by 2024 that return had risen to slightly over $10.

Other benefits and harms we cannot specify: Consumer confidence in financial institutions has not improved, but the CFPB’s role in this, if any, is not evident. The great recession 2007 - 2010 left US consumers with little confidence in banks and other financial institutions, and little confidence that the federal governemnt would protect them from predatory banks and businesses. The University of Michigan annual survey shows the Federal Reserve, commercial banks, brokerages and mutual funds, and insurance companies are viewed with deep and very well-deserved mistrust, and no evident trajectory of strengthening trust. (2023 survey data - the most recent data were collected in the immediate aftermath of the collapse of Silicon Valley Bank and two smaller banks, in March 2023 and the subsequent 25 basis point rate hike from the Federal Reserve. It is not clear that this survey has continued beyond 2023.)

Notes

- The CAGR calculations above do not account for inflation.The 6.2% CAGR in CFPB operating budget is slight given that background inflation accounted for 4.9% per year. The Bureau’s budget has risen annually by about 1.3% in real spending power. (In practice this is deliberate. The budget is constrained by a cap imposed at the Federal Reserve.)

- Sources: mostly the CFPB itself, HERE and HERE and HERE (the 2024 annual report). Also the Congressional Research Report HERE.

This Calx Quick Dip note was created by a combination of human research (reading CFPB papers still online, plus Google search of news reports, etc), augmented by Perplexity Pro building the ROI table. We welcome input, and critique, particularly from financial services and regulatory theory experts, activists and economists.

Comments ()